Is It Too Late to Build Wealth After 40?

Reaching your 40s can trigger a financial reality check. Maybe your retirement savings aren’t where you expected them to be. Perhaps life events such as divorce, career changes, or raising children slowed your ability to save earlier in life. Or maybe you simply didn’t start investing until recently.

Whatever the reason, many people find themselves asking a version of the same question:

Is it too late to build wealth after 40?

The short answer is no. In fact, for many people their 40s and 50s are the most powerful years for wealth accumulation. Income tends to peak during these decades, investment contributions can increase dramatically, and compound growth still has meaningful time to work.

Building wealth after 40 requires a focused strategy, but it is far from impossible. This guide explores how investing later in life works, how to catch up on retirement savings, and the practical steps that can help you build long-term financial security.

Why People Start Investing Later in Life

While financial advice often emphasizes starting early, many people don’t begin serious investing until midlife.

There are several common reasons.

Career development takes time

Many careers require years of training or early-stage income growth before meaningful savings become possible. Professionals such as doctors, lawyers, entrepreneurs, and small business owners often see their highest income levels later in life.

Family expenses dominate early adulthood

During their 20s and 30s, people often face major expenses including:

student loans

childcare

housing purchases

relocation costs

career transitions

These costs can delay aggressive investing.

Life transitions

Divorce, job loss, and other life changes can temporarily interrupt financial progress. Starting over financially after a major life event is more common than many people realize. The key takeaway is that starting later doesn’t eliminate the possibility of building wealth.

The Advantage of Investing After 40

Although starting early has clear benefits, people in their 40s often have advantages that younger investors don’t.

Higher income potential

Many professionals reach peak earnings in their 40s and 50s. Higher income can allow larger investment contributions than were possible earlier.

Greater financial clarity

By midlife, people often have a clearer understanding of their financial priorities and lifestyle needs. This clarity can lead to more disciplined financial decisions.

Fewer early-life expenses

Expenses such as childcare or student loan payments may begin to decline during this stage of life. That frees up more money for saving and investing. Because of these factors, many people accelerate wealth building significantly after 40.

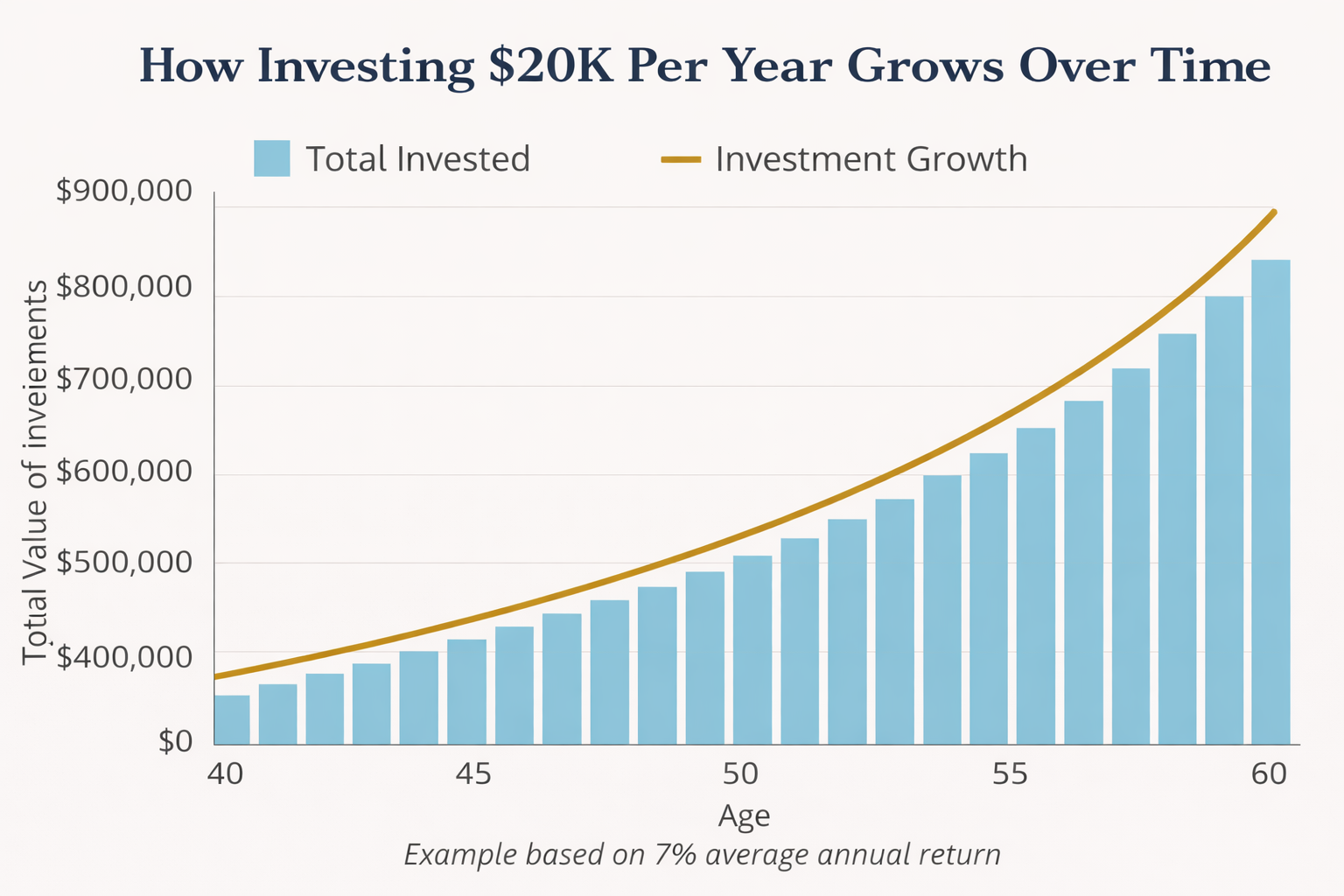

How Much Time Do You Really Have?

One common concern among late starters is that there isn’t enough time for investments to grow. But even starting at 40 leaves several decades for compounding.

Consider the following example.

If someone invests $20,000 per year starting at age 40 and earns an average return of 7%, their investments could grow to approximately:

$820,000 by age 60

If contributions increase to $30,000 per year, the portfolio could grow to roughly:

$1.2 million by age 60

While starting earlier would produce larger totals, these numbers demonstrate that significant wealth accumulation is still possible later in life.

Retirement Savings Benchmarks

Many financial planners provide benchmarks for retirement savings based on income.

These guidelines can help assess whether your savings are on track.

Age Suggested Retirement Savings

30 1× annual salary

40 3× salary

50 6× salary

60 8–10× salary

If your savings fall below these benchmarks, you may need to increase contributions or adjust retirement expectations. However, these guidelines are only rough estimates. Personal circumstances, spending needs, and retirement age all affect how much you actually need to save.

Catch-Up Retirement Contributions

One important advantage for people over 50 is the availability of catch-up contributions. These allow individuals to invest additional funds in retirement accounts beyond standard limits.

For example, in many retirement plans:

401(k) plans

Individuals over age 50 can contribute additional catch-up amounts beyond the regular annual limit.

Individual Retirement Accounts (IRAs)

Catch-up contributions allow slightly higher annual contributions for individuals over 50.

These additional contributions can significantly accelerate retirement savings during your highest-earning years.

The Power of Saving Rate

When starting later, your savings rate becomes especially important. The percentage of income you invest each year often matters more than the age at which you begin.

For example:

Savings Rate Financial Impact

10% of income Slow wealth growth

20% of income Moderate growth

30–40% of income Rapid wealth building

Individuals pursuing financial independence often save 25–40% of income during peak earning years. Higher savings rates can compensate for a later start.

Investment Strategy After 40

When investing after 40, a balanced strategy is typically recommended. Because retirement may still be decades away, investments usually include growth assets such as stocks.

A typical diversified portfolio might include:

U.S. stock index funds

international equity funds

bond funds

dividend-producing investments

Diversification helps manage risk while still allowing the portfolio to grow over time.

Avoiding Common Late-Start Investing Mistakes

People trying to catch up financially sometimes make mistakes that can undermine long-term results.

Taking excessive investment risk

Some investors attempt to compensate for a late start by making highly speculative investments. However, large losses can be difficult to recover from later in life. Maintaining a diversified portfolio is generally a safer long-term strategy.

Trying to time the market

Market timing is notoriously difficult. Consistent investing over time usually produces better results than attempting to predict market movements.

Ignoring retirement accounts

Tax-advantaged accounts such as 401(k)s and IRAs offer significant benefits. Maximizing these accounts can improve long-term investment growth.

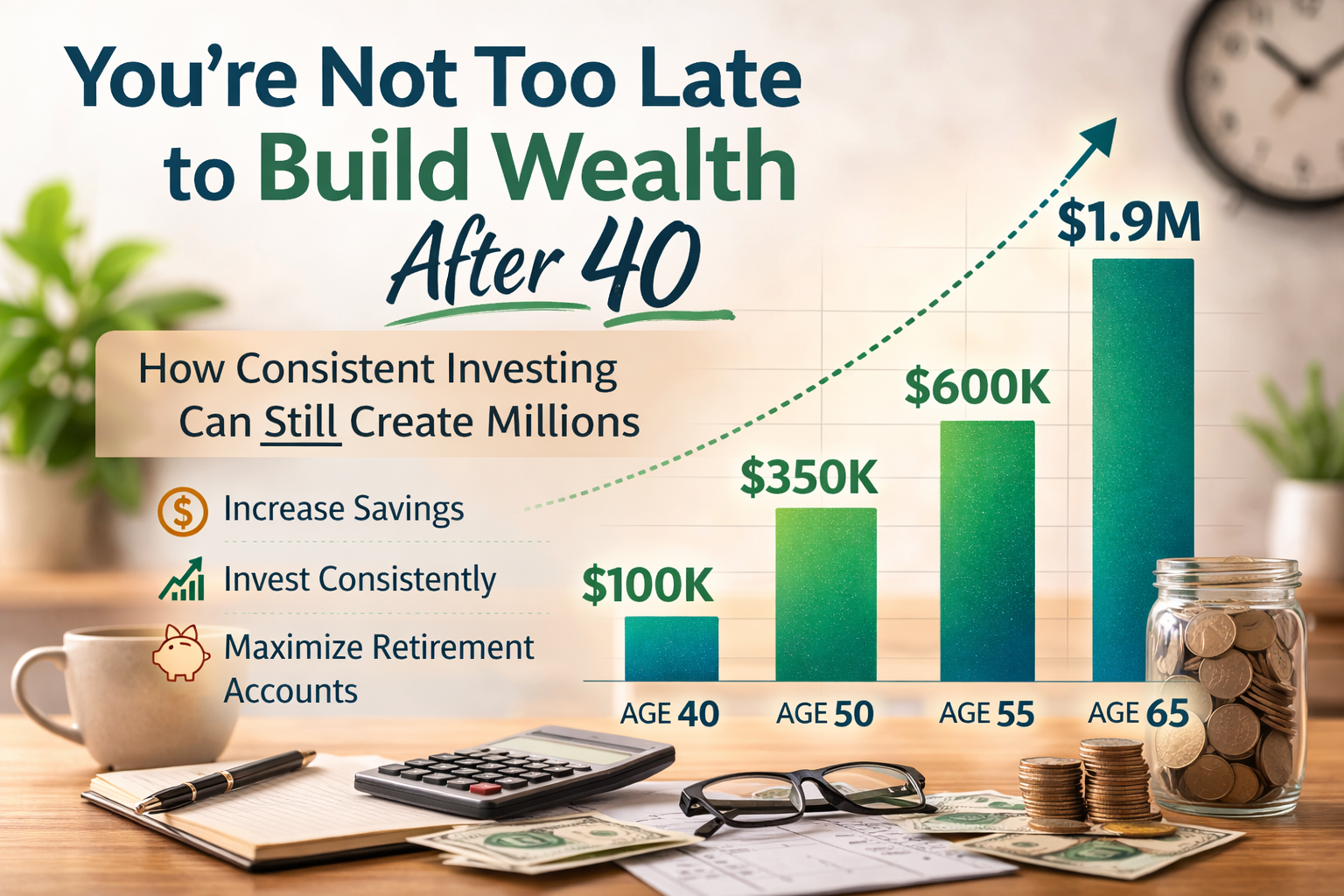

Scenario Modeling: Building Wealth After 40

To understand how investing after 40 can work, consider several simplified scenarios.

Scenario 1: Moderate saver

Age: 40

Annual investment: $15,000

Average return: 7%

Portfolio value at 65:

~$950,000

Scenario 2: Aggressive saver

Age: 40

Annual investment: $30,000

Average return: 7%

Portfolio value at 65:

~$1.9 million

Scenario 3: Late start but high income

Age: 45

Annual investment: $40,000

Average return: 7%

Portfolio value at 65:

~$1.6 million

These examples show that wealth accumulation remains very possible with disciplined investing.

Adjusting Retirement Expectations

If you begin investing later in life, it may help to adjust retirement expectations slightly. Possible adjustments include:

retiring a few years later

reducing future living expenses

relocating to lower-cost areas

supplementing retirement income with part-time work

Even small changes can significantly improve financial sustainability.

The Role of Social Security

Social Security benefits play a significant role in retirement income for many households. Benefits vary depending on lifetime earnings and the age at which they are claimed. Delaying benefits increases monthly payments. For example, claiming benefits at age 70 instead of 62 can increase monthly income significantly.

When combined with personal savings, Social Security can help create a more stable retirement income stream.

Reducing Debt Before Retirement

Another important step in building wealth after 40 is reducing debt. High-interest debt can slow financial progress by diverting income away from investing.

Common priorities include:

paying off credit cards

reducing personal loans

managing mortgage debt strategically

Lower debt levels improve financial flexibility and make saving easier.

Housing and Wealth Building

Housing decisions can also influence long-term financial outcomes. For some people, owning a home can build equity over time. For others, renting and investing the difference may provide greater flexibility.

The key factor is ensuring that housing costs remain aligned with long-term financial goals. Overspending on housing can limit the amount available for investing.

A Practical Plan to Build Wealth After 40

If you want to accelerate wealth building in midlife, consider focusing on a few key priorities.

Increase savings: Gradually increase the amount you invest each year.

Maximize retirement accounts: Take full advantage of tax-advantaged retirement accounts whenever possible.

Invest consistently: Regular contributions help smooth out market volatility.

Maintain long-term discipline: Wealth building is a long-term process that rewards patience.

Final Thoughts

Starting to invest after 40 may feel late compared with traditional financial advice, but it is far from hopeless. In many cases, midlife can become the most productive period for wealth building. Higher income, greater financial clarity, and disciplined investing can allow significant progress over the next several decades.

The most important step is simply beginning. Even if you feel behind today, consistent investing and thoughtful financial decisions can still create meaningful financial security for the future. Building wealth after 40 isn’t about perfection. It’s about steady progress over time.