Renting vs Buying in Your 40s: What Actually Makes Sense?

Housing is usually the largest expense in most households. By the time people reach their 40s, many have already bought a home, sold one, moved cities, or reconsidered where and how they want to live.

But midlife often brings major transitions that make housing decisions more complicated.

Divorce, career changes, relocating for work, or simply wanting more flexibility can all lead people to reconsider whether renting or buying makes the most financial sense.

Conventional wisdom often suggests that buying a home is always the better long-term financial choice. But that assumption doesn’t always hold up when you examine the numbers closely.

In some cases, renting can actually be the smarter financial decision, especially during periods of life transition.

Why Housing Decisions in Your 40s Are Different

Buying a home in your 20s or early 30s often comes with a long timeline. Someone who purchases a house at 28 might reasonably expect to live there for several decades.

In your 40s, however, the timeline becomes less predictable. Several life factors may influence housing decisions at this stage:

career pivots

family changes

children leaving home in the future

geographic flexibility

financial independence planning

Because of these uncertainties, flexibility can become more valuable than it was earlier in life.

That’s one reason many people begin asking a different question:

Is renting actually better than buying in some situations?

The Traditional Argument for Buying

The most common argument for buying a home is that it builds equity. When you make mortgage payments, a portion of the payment goes toward the principal balance, gradually increasing your ownership stake in the property. Over time, homeowners may benefit from:

property appreciation

principal paydown

tax deductions in some cases

stability in housing costs

If someone owns a home for 15–30 years in a strong housing market, the financial benefits can be significant. However, this outcome depends heavily on how long the home is held and how housing markets perform. Shorter timelines often produce very different financial results.

The Hidden Costs of Homeownership

When people compare renting and buying, they often focus primarily on monthly payments. But the true cost of owning a home includes more than just a mortgage. Homeowners typically pay for:

property taxes

homeowners insurance

maintenance and repairs

HOA fees in some communities

closing costs when buying and selling

Maintenance alone is often estimated at 1–2% of a home’s value annually. For a $500,000 home, that could mean $5,000 to $10,000 per year in maintenance costs. These additional expenses can significantly change the financial comparison between renting and buying.

Using a Rent vs Buy Calculator

A rent vs buy calculator can help estimate the long-term cost difference between renting and purchasing a home.

These calculators typically consider variables such as:

home purchase price

down payment

mortgage interest rate

property taxes

insurance

maintenance costs

rent increases over time

investment returns on savings

One of the most important variables is how long you plan to stay in the home. If someone sells a home within five years, closing costs and real estate commissions can significantly reduce the financial advantage of ownership.

In contrast, homeowners who stay in a property for 10–20 years often benefit more from appreciation and mortgage paydown.

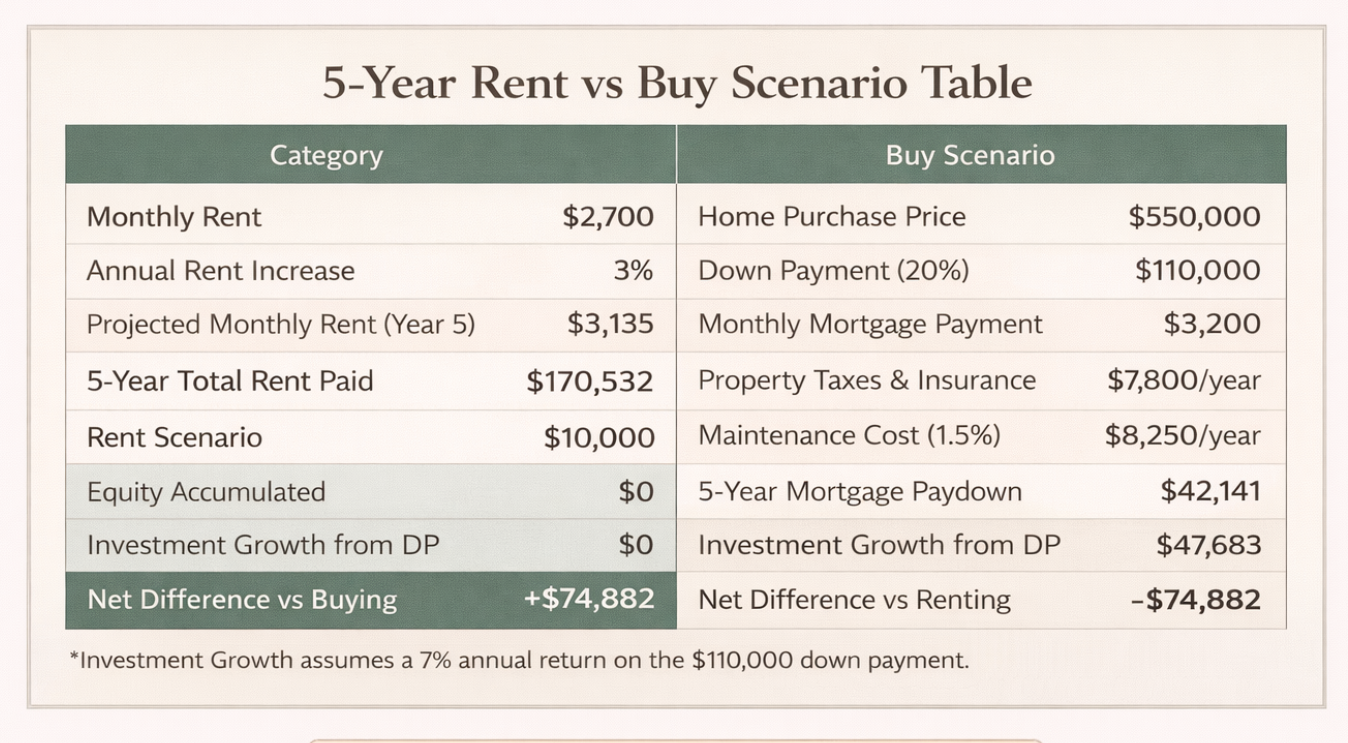

A Simple Long-Term Cost Example

Consider a simplified example comparing renting and buying.

Scenario A: Renting

Monthly rent: $2,700

Annual rent: $32,400

If rent increases 3% annually, housing costs gradually rise over time.

However, renters may invest savings that would otherwise go toward:

down payments

property taxes

maintenance

Those investments can grow over time.

Scenario B: Buying

Home price: $550,000

Down payment: $110,000

Mortgage payment: $3,200 per month

Additional costs:

Property taxes: $6,000/year

Insurance: $1,800/year

Maintenance: $7,000/year

Total annual housing cost could approach $50,000 per year.

In this example, owning the home costs significantly more each year than renting. However, the homeowner is also building equity. The key question becomes whether that equity growth outweighs the additional costs.

Opportunity Cost of a Down Payment

Another factor that often gets overlooked is opportunity cost.

When you purchase a home, your down payment becomes tied up in the property. For example, a $120,000 down payment invested in a diversified stock portfolio earning an average 7% annual return could grow substantially over time.

Over 20 years, that investment could grow to approximately $465,000. This doesn’t necessarily mean renting is always better, but it illustrates that housing decisions involve trade-offs. Money used for a down payment could otherwise be invested.

Lifestyle Flexibility

Beyond financial modeling, renting and buying also involve lifestyle considerations. In midlife, flexibility can be especially valuable. Renting allows people to:

move cities more easily

adjust housing size as family needs change

avoid large repair costs

relocate for career opportunities

This flexibility can be particularly useful during periods of transition. For example, someone considering a career change, relocation, or major life adjustment may prefer the flexibility of renting.

Stability and Emotional Factors

On the other hand, owning a home offers a different kind of stability. Homeownership can provide:

long-term housing security

control over renovations and customization

predictable mortgage payments over time

a sense of permanence

For families with children, stability may be an important consideration. Staying in one home can provide consistency in school districts and community relationships. These emotional and lifestyle factors often play a meaningful role in housing decisions.

Housing Market Risk

Real estate markets can rise and fall over time. While long-term appreciation has historically occurred in many markets, short-term fluctuations can create risk for homeowners who need to sell quickly.

If housing prices decline shortly after a purchase, homeowners may face the possibility of selling at a loss. Renters avoid this type of market risk entirely.

This is one reason renting can be appealing during uncertain economic periods.

Renting as a Strategic Choice

In recent years, renting has increasingly been viewed as a strategic choice rather than a financial failure.

Many financially secure individuals choose to rent for reasons including:

geographic mobility

lower maintenance responsibilities

ability to invest more aggressively

avoiding real estate concentration risk

For someone pursuing financial independence, renting can sometimes allow more money to be invested in diversified assets. This approach prioritizes investment growth over property ownership.

When Buying Makes More Sense

Despite the advantages of renting, there are many situations where buying can be the better financial choice.

Buying may make sense when:

you expect to stay in the home long-term

housing prices are relatively affordable compared to rents

mortgage rates are favorable

you value stability and customization

In these cases, long-term appreciation and mortgage paydown can create meaningful wealth over time.

Homeownership can also act as a form of forced savings for some households.

Questions to Ask Before Deciding

If you’re evaluating renting versus buying in your 40s, several questions can help clarify the decision.

How long do you expect to stay?

The longer you stay in a home, the more likely ownership becomes financially advantageous.

How stable is your career or location?

If you may move within a few years, renting may reduce financial risk.

What are housing costs relative to income?

Housing expenses that consume too much of your income can limit savings and investment opportunities.

How important is flexibility?

Flexibility becomes especially valuable during life transitions.

The Bigger Financial Picture

Housing decisions should ideally be evaluated within the context of your broader financial plan. For example, someone focused on building investment assets or pursuing financial independence may prioritize maximizing investment contributions. In that case, renting may allow more money to flow into investments.

Alternatively, someone who values long-term housing stability may find homeownership aligns better with their goals. Both paths can lead to financial security.

Final Thoughts

The debate between renting and buying often gets framed as a simple financial calculation. But in reality, the decision involves both financial and lifestyle factors. Buying a home can create long-term wealth through appreciation and mortgage paydown. Renting can offer flexibility, lower risk, and the ability to invest more aggressively.

In your 40s, the best housing choice often depends on where you are in life. Periods of transition may favor renting, while long-term stability may favor buying. Instead of assuming one option is always superior, it can be more helpful to analyze the trade-offs carefully.

Housing is one of the biggest financial decisions most people make. Approaching it thoughtfully can help ensure that your housing choice supports both your financial goals and your lifestyle priorities.