Can You Retire With $500K?

Many people reach midlife and begin asking a deceptively simple question:

Is $500,000 enough to retire?

On the surface, half a million dollars sounds like a significant amount of money. But retirement planning depends heavily on several variables, including your age, annual spending, investment strategy, and expected lifespan.

For some people, $500,000 may support retirement comfortably. For others, it may only cover a portion of their future expenses. The difference often comes down to how retirement income works. Instead of focusing only on the total savings amount, it helps to evaluate how those savings translate into sustainable annual income.

This article explores whether you can realistically retire with $500K by examining:

retirement withdrawal strategies

spending assumptions

retirement age differences

investment returns

lifestyle adjustments

The goal isn’t to provide a single universal answer. Instead, it’s to understand the conditions under which $500,000 could support retirement, and when it may fall short.

How Retirement Income Actually Works

One of the most common misconceptions about retirement savings is that people spend their entire savings balance over time. In reality, retirement income typically comes from withdrawals from invested assets.

These assets might include:

retirement accounts (401(k), IRA)

brokerage accounts

dividend-paying investments

bond funds or other income-producing assets

Because these investments remain invested during retirement, they can continue generating returns while withdrawals are made.

This is where withdrawal strategies become important.

The 4% Rule: A Starting Point

A common guideline in retirement planning is the 4% rule. This rule suggests that retirees can withdraw approximately 4% of their portfolio in the first year of retirement, adjusting that amount for inflation each year. The idea is that a diversified investment portfolio has historically been able to sustain withdrawals at that level for about 30 years.

Using this guideline, a $500,000 portfolio could potentially generate:

$20,000 per year

(4% of $500,000)

While this amount might cover basic living expenses in some situations, it would likely be insufficient for many households without additional income sources. However, the 4% rule is only a rough estimate and may not apply to every situation.

What $500K Could Provide in Retirement Income

Below is a simplified look at how a $500,000 portfolio might translate into annual income under different withdrawal assumptions.

Withdrawal Rate Annual Income

3% $15,000

4% $20,000

5% $25,000

Higher withdrawal rates provide more income in the short term but increase the risk of running out of money later in retirement. Lower withdrawal rates tend to make retirement savings last longer.

Why Retirement Age Matters

One of the biggest factors in determining whether $500K is enough to retire is when retirement begins.

A portfolio must last significantly longer if someone retires at 45 compared to retiring at 65.

For example:

Retirement Age Possible Retirement Length

45 40–45 years

55 30–35 years

65 20–30 years

A longer retirement means a portfolio must support withdrawals for a much longer period of time.

Because of this, someone retiring earlier typically needs either:

a larger portfolio

a lower withdrawal rate

additional income sources

Scenario Modeling: Retiring With $500K

To better understand how $500K might support retirement, it helps to examine a few hypothetical scenarios. These examples illustrate how spending levels and retirement age affect sustainability.

Scenario 1: Early Retirement at 45

Savings: $500,000

Withdrawal rate: 3%

Annual income: $15,000

At this level, the portfolio generates relatively limited income. Someone retiring at 45 with $500K would almost certainly need additional income sources such as:

part-time work

rental income

business income

spouse income

Healthcare costs also become a major consideration, since Medicare eligibility typically begins at age 65.

In most cases, $500K alone would not support full retirement at age 45 without substantial lifestyle adjustments.

Scenario 2: Retirement at 55

Savings: $500,000

Withdrawal rate: 4%

Annual income: $20,000

At this stage, the portfolio could potentially cover a portion of living expenses. However, most households would still need additional income streams. Some retirees bridge the gap with:

part-time consulting

Social Security beginning later

downsizing housing

reduced spending

This type of “semi-retirement” has become increasingly common.

Scenario 3: Retirement at 65

Savings: $500,000

Withdrawal rate: 4%

Annual income: $20,000

At age 65, the situation often looks different because additional income sources may become available. For example:

Social Security benefits might provide:

$1,500–$2,500 per month depending on earnings history.

If someone receives $2,000 per month from Social Security:

Annual Social Security income: $24,000

Combined with portfolio withdrawals:

Portfolio income: $20,000

Social Security: $24,000

Total annual income: $44,000

For many households, this could support a modest but workable retirement.

Recommended: How Much Should You Have Saved by Age?

Spending Assumptions Matter

Perhaps the most important factor in determining whether $500K is enough to retire is annual spending.

Some retirees spend relatively little due to:

paid-off housing

low cost of living areas

minimal debt

simpler lifestyles

Others may spend significantly more. Below are rough examples of how spending affects sustainability.

Annual Spending Portfolio Needed (4% Rule)

$30,000 $750,000

$40,000 $1,000,000

$60,000 $1,500,000

$80,000 $2,000,000

This table illustrates why many retirement planners suggest aiming for $1 million or more in retirement savings. However, not everyone needs the same level of spending.

Geographic Cost Differences

Where you live in retirement can significantly influence whether $500K is sufficient. Living costs vary dramatically across different regions. In lower-cost areas, $40,000 per year may cover housing, food, transportation, and healthcare. In high-cost metropolitan areas, that same amount might not cover basic living expenses.

Some retirees relocate to lower-cost regions in order to stretch retirement savings further.

Housing Costs in Retirement

Housing is typically the largest expense in most retirement budgets. Retirees who have fully paid off their homes may require significantly less annual income.

For example, someone with a paid-off home might only need to cover:

property taxes

insurance

maintenance

utilities

In contrast, retirees who continue renting or paying a mortgage may face significantly higher monthly expenses.

Reducing housing costs can dramatically improve retirement sustainability.

Healthcare Costs

Healthcare becomes an increasingly important expense in retirement. Although Medicare begins at age 65, it does not cover every medical cost. Retirees may still need to pay for:

Medicare premiums

supplemental insurance

prescriptions

long-term care expenses

Healthcare costs can increase significantly later in life, which is another reason many planners prefer conservative withdrawal rates.

Investment Strategy After Retirement

Even after retiring, most portfolios remain invested. A diversified retirement portfolio might include:

stock index funds

bond funds

dividend-paying stocks

cash reserves

Growth investments help offset inflation and allow the portfolio to continue generating returns over time. Without investment growth, retirement savings could lose purchasing power over decades.

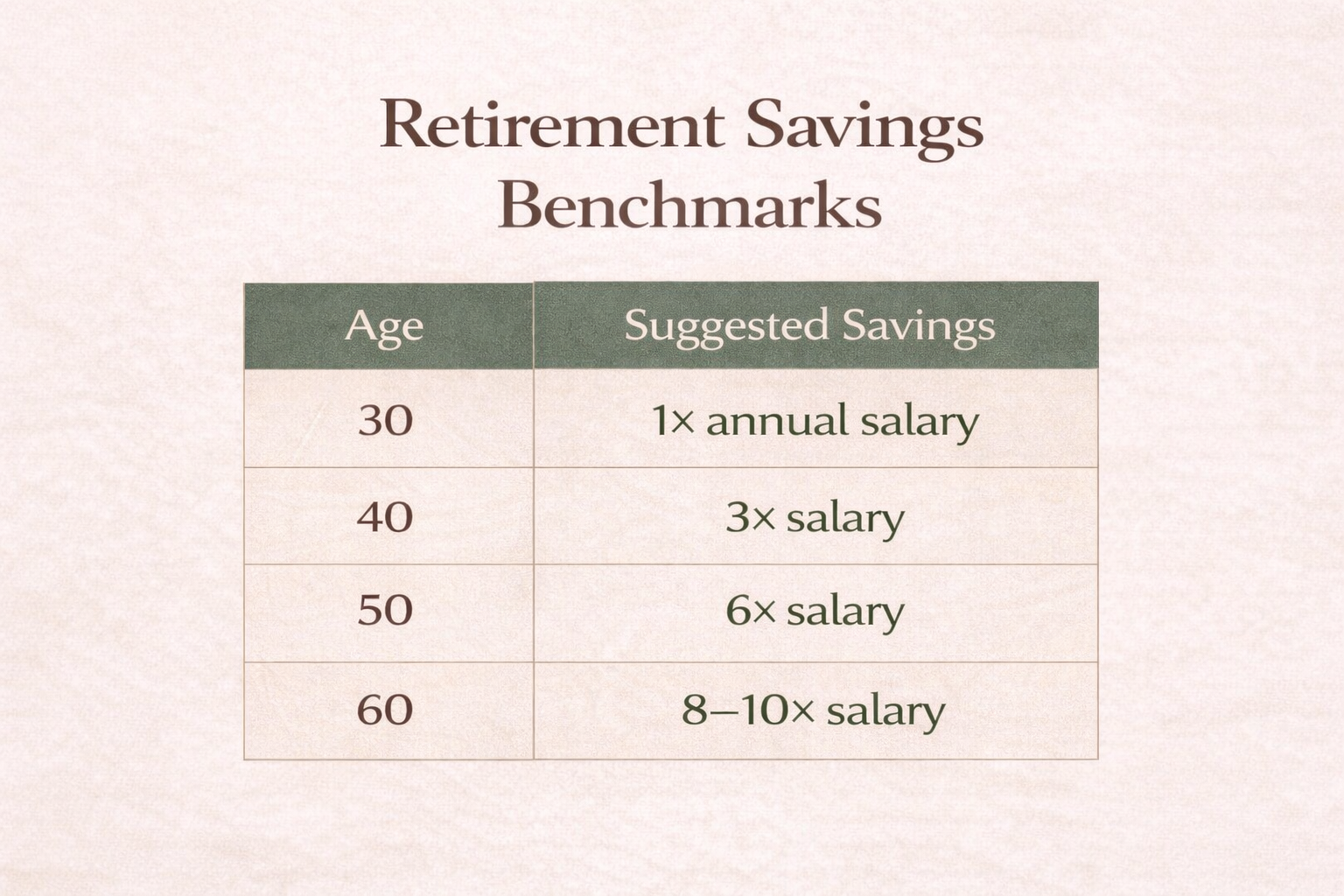

Retirement Savings Benchmarks

Many financial planners provide benchmarks for retirement savings based on income.

For example, a commonly cited guideline suggests:

These benchmarks are general guidelines rather than strict requirements.

Someone with lower expected retirement spending may not need as much savings as these benchmarks suggest.

Strategies to Stretch $500K Further

If $500K is your primary retirement savings amount, several strategies may help extend its longevity.

Delay Social Security

Waiting until age 70 to claim Social Security increases monthly benefits significantly. Higher benefits can reduce reliance on portfolio withdrawals.

Reduce Fixed Expenses

Lowering recurring costs — particularly housing — can significantly reduce retirement income needs.

Continue Part-Time Work

Many retirees choose to work part-time, either for income or personal fulfillment. Even modest income can reduce pressure on retirement savings.

Maintain Investment Growth

Keeping part of the portfolio invested in equities can help offset inflation over long retirement periods.

The Bigger Picture

Retirement planning often focuses heavily on a single number. But the reality is that retirement outcomes depend on multiple interacting factors. These include:

spending levels

retirement age

investment performance

health and longevity

additional income sources

For some individuals, $500K could support a modest retirement combined with Social Security and careful budgeting. For others, it may represent only part of the required savings.