How Much Money Do You Need to Retire at 45?

Retiring at 45 is a dream for many people who want more control over their time, work, and lifestyle. The idea of leaving traditional employment decades before the typical retirement age can feel both exciting and intimidating.

But early retirement isn’t simply about saving aggressively. It requires careful financial planning, realistic assumptions about expenses, and a clear understanding of how investment income works over long periods of time.

In traditional retirement planning, people expect to stop working around age 65. Retiring at 45 means your investments may need to support 40–50 years of living expenses, which dramatically changes the math.

This guide will walk through the key questions behind early retirement, including:

How financial independence actually works

How much money you may need to retire at 45

The math behind withdrawal rates

Lifestyle tradeoffs to consider

Tools and calculators that can help you estimate your own numbers

Early retirement is possible for some people, but it requires thoughtful planning and realistic expectations.

What Does Retiring at 45 Really Mean?

When people talk about retiring early, they’re often referring to financial independence. Financial independence means having enough invested assets to cover your living expenses without relying on traditional employment income.

Your investments generate income through:

dividends

interest

investment withdrawals

capital gains

Instead of working for a paycheck, your assets provide the income needed to support your lifestyle.

For example:

If you spend $60,000 per year, your investment portfolio would need to generate approximately that amount annually.

However, determining how large that portfolio must be depends on withdrawal strategies and market assumptions.

The Math Behind Early Retirement

One of the most widely discussed concepts in early retirement planning is the 4% rule.

The 4% rule comes from retirement research examining how long a diversified investment portfolio might last when withdrawals begin.

The basic idea is simple:

You withdraw 4% of your portfolio in the first year of retirement, then adjust that amount for inflation each year.

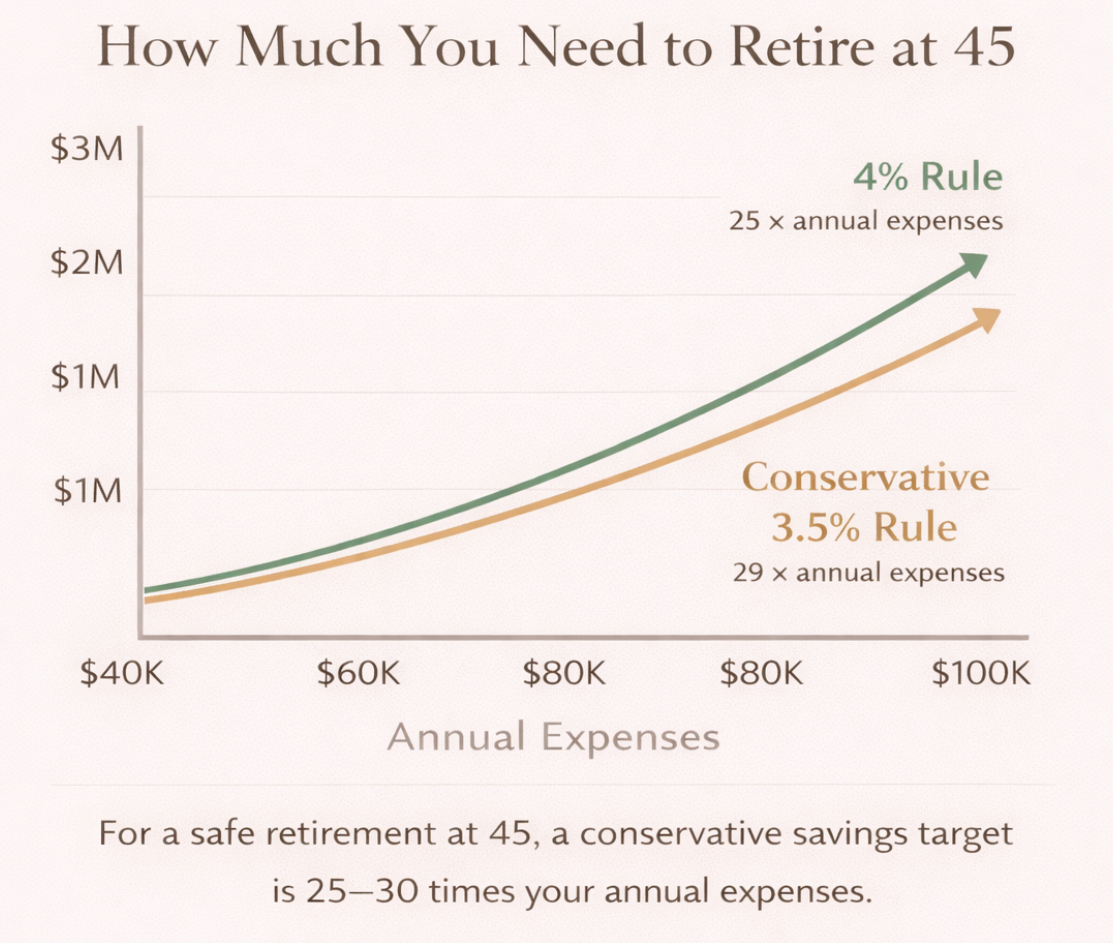

Using this guideline, the required portfolio size can be estimated using a simple formula:

Annual expenses × 25 = Portfolio target

This is sometimes called the “25x rule.”

For example:

Annual Spending Portfolio Needed

$40,000 $1,000,000

$60,000 $1,500,000

$80,000 $2,000,000

$100,000 $2,500,000

This calculation provides a starting estimate for financial independence.

However, retiring at 45 introduces additional complexity.

Why Retiring at 45 Requires More Planning

The 4% rule was originally designed around 30-year retirement horizons, assuming retirement around age 65.

Retiring at 45 may require your portfolio to last 45 years or longer.

Because of this longer timeline, some financial planners recommend a more conservative withdrawal rate, such as:

3.5%

3.25%

3%

Using a lower withdrawal rate means you need a larger investment portfolio to safely support early retirement.

For example:

Annual Spending Portfolio Needed (3.5%)

$40,000 $1,140,000

$60,000 $1,700,000

$80,000 $2,285,000

$100,000 $2,850,000

While the difference between 4% and 3.5% may appear small, it significantly increases the required savings.

How an Early Retirement Calculator Helps

An early retirement calculator allows you to estimate how long your portfolio might last based on several variables.

Most calculators consider factors such as:

current savings

annual spending

investment returns

withdrawal rate

inflation

These tools help visualize how different choices affect your financial independence timeline.

For example, increasing your annual savings or reducing your expected retirement spending can significantly change the timeline.

Even small adjustments in spending assumptions can dramatically affect the amount of money needed to retire.

A Simple Financial Independence Example

Consider a hypothetical scenario.

A household wants to retire at age 45 and expects annual expenses of $70,000.

Using the 4% rule:

$70,000 × 25 = $1.75 million portfolio

If they prefer a more conservative 3.5% withdrawal rate:

$70,000 ÷ 0.035 = $2 million portfolio

The difference between the two strategies is roughly $250,000 in additional savings.

This illustrates how sensitive early retirement planning can be to withdrawal assumptions.

Key Factors That Affect Early Retirement

Retiring at 45 isn’t only about hitting a specific savings target.

Several additional factors influence whether early retirement is sustainable.

Investment Strategy

A diversified investment portfolio typically includes a mix of:

stock index funds

bond funds

international equities

dividend investments

Because early retirees may rely on investment income for decades, portfolio stability becomes particularly important.

Healthcare Costs

Healthcare is one of the biggest challenges for early retirees in the United States.

Medicare eligibility typically begins at age 65, leaving a 20-year gap for someone retiring at 45.

Early retirees must plan for private health insurance or other coverage options.

Healthcare costs alone can significantly increase the amount of savings needed.

Inflation

Inflation erodes purchasing power over time.

If your retirement lasts 40 years, the cost of living could increase substantially during that period.

This is why most early retirement plans assume long-term investment growth that outpaces inflation.

Lifestyle Tradeoffs of Early Retirement

Retiring at 45 often involves lifestyle choices that differ from traditional career paths.

Understanding these tradeoffs can help clarify whether early retirement is realistic for your situation.

Spending Flexibility

Many early retirees maintain the option to adjust spending if market conditions change.

For example, they might:

reduce travel spending during market downturns

delay large purchases

supplement income with part-time work

Flexibility helps reduce the risk of depleting investments too quickly.

Location Choices

Cost of living plays a major role in early retirement feasibility.

Someone spending $40,000 annually in a lower-cost region may reach financial independence much sooner than someone spending $100,000 in a major city.

Housing costs alone can dramatically affect the timeline.

Purpose and Lifestyle

Retirement at 45 doesn’t necessarily mean doing nothing.

Many early retirees pursue activities such as:

consulting or freelance work

passion projects

volunteering

starting small businesses

Financial independence often provides flexibility rather than complete inactivity.

Can You Still Work After Retiring Early?

Many people pursuing financial independence plan to continue working in some capacity.

This approach is sometimes called “semi-retirement.”

For example, someone might:

leave a high-stress career

transition to part-time work

pursue lower-income but more fulfilling work

Even modest income during early retirement can significantly reduce pressure on investment portfolios.

For example, earning $20,000 annually could reduce required portfolio withdrawals by the same amount.

That income can dramatically improve portfolio sustainability.

Recommended: How to Start a Blog and Earn Income

How to Start Planning for Early Retirement

If retiring at 45 is a long-term goal, several steps can help move you toward financial independence.

Track Your Current Spending

Understanding your spending habits provides a realistic estimate of future retirement expenses.

Many people underestimate how much they spend each year.

Increase Your Savings Rate

Your savings rate plays a major role in how quickly you reach financial independence.

Saving 20–30% of income can dramatically accelerate the process.

Some early retirement advocates save even more during high-income years.

Invest Consistently

Regular investment contributions allow compounding to work over time.

Broad stock market index funds are often used as core portfolio holdings because they provide diversification and long-term growth potential.

Avoid Lifestyle Inflation

As income increases, lifestyle inflation can quietly increase spending.

Maintaining moderate living expenses while income grows allows more money to be invested.

Is Retiring at 45 Realistic?

For some people, retiring at 45 is achievable. For others, it may not align with financial goals or lifestyle preferences.

Several factors influence feasibility:

income level

savings rate

spending habits

investment performance

cost of living

healthcare costs

Rather than focusing only on a specific age, many people pursue financial independence because it provides flexibility and optionality.

Reaching financial independence means work becomes a choice rather than a necessity.

That freedom can be valuable even if someone chooses to continue working in some capacity.

Final Thoughts

Retiring at 45 requires thoughtful financial planning and a clear understanding of long-term investment sustainability.

While simple guidelines such as the 4% rule provide useful starting points, early retirement involves additional factors including healthcare costs, inflation, and lifestyle choices.

The exact amount needed to retire will vary widely depending on individual spending habits and investment strategies.

For many people, the goal of financial independence is less about leaving work entirely and more about creating greater control over how they spend their time.

With careful planning, consistent investing, and realistic expectations, early retirement can become a meaningful long-term goal rather than just an abstract idea.