How Much Net Worth Should You Have at 40? A Realistic Benchmark Guide

Many people reach their late 30s or early 40s and begin asking a simple but loaded question:

“Am I on track financially?”

Often, this question is framed around net worth. You may have heard benchmarks suggesting that by age 40 you should have a certain multiple of your income saved or invested. Financial institutions, retirement planners, and media outlets frequently publish guidelines that attempt to define where you “should” be financially at different ages.

But real life rarely fits neatly into benchmarks.

By the time people reach their 40s, they’ve often experienced career shifts, housing decisions, family changes, divorce, or periods of financial instability. These factors can dramatically affect net worth in ways that standard formulas don’t account for.

The goal isn’t to judge where you are financially. It’s to help you understand your trajectory and make smarter decisions going forward.

What Is Net Worth?

Your net worth is simply the difference between what you own and what you owe.

Assets may include:

Cash and savings accounts

Investment accounts (brokerage accounts, IRAs, 401(k)s)

Home equity

Retirement accounts

Business ownership or other investments

Liabilities may include:

Mortgage debt

Credit card balances

Student loans

Auto loans

Personal loans

Your net worth is calculated as:

Assets – Liabilities = Net Worth

For example, if you have:

$350,000 in investments

$100,000 in home equity

$50,000 in savings

And you owe:

$200,000 on a mortgage

Your net worth would be:

$500,000 – $200,000 = $300,000

Net worth is one of the simplest ways to measure financial progress because it captures your overall financial position.

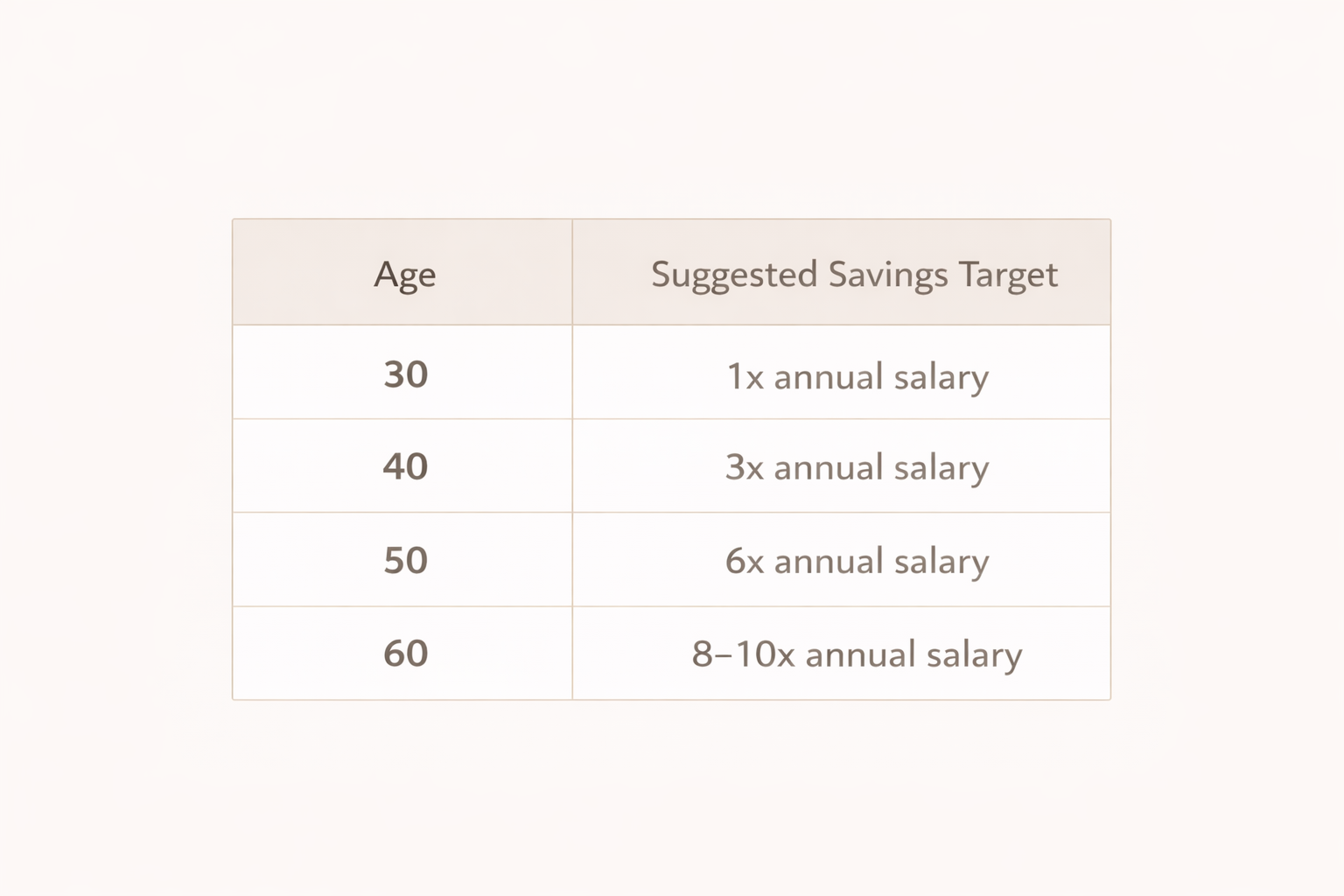

Common Net Worth Benchmarks for Age 40

Several financial institutions publish savings or net worth benchmarks by age.

One of the most widely cited guidelines comes from Fidelity Investments, which suggests the following savings multiples:

Under this framework, someone earning $100,000 per year should ideally have about $300,000 saved or invested by age 40. Other financial planners offer similar guidelines.

For example:

$200,000–$300,000 net worth is often cited as a typical target for middle-income households by 40.

Higher earners may aim for $500,000 or more by that age.

These benchmarks provide a useful starting point. They are based on the assumption that someone is saving consistently throughout their career and plans to retire around age 65.

However, these numbers assume a relatively stable financial path.

In reality, financial lives are rarely that predictable.

Why Net Worth Benchmarks Can Be Misleading

Benchmarks can be helpful for rough comparisons, but they don’t always reflect the complexities of real life. Several factors can significantly affect net worth by age 40.

Career Trajectory

Income often grows significantly during a person’s 30s and 40s.

Someone earning $70,000 at age 30 might earn $130,000 by age 40. That increase may lead to rapid savings growth later in life.

In this case, a lower net worth at 40 doesn’t necessarily indicate a problem. Future earning power may compensate.

Divorce or Relationship Changes

Divorce can dramatically affect net worth due to:

Asset division

Legal costs

Changes in housing arrangements

Reduced household income

Someone who goes through a divorce in their late 30s may see their net worth temporarily decline, even if they were previously on track.

Late Career Growth

Some professions have slow early earnings but strong later income potential.

Examples include:

Physicians

Lawyers

Entrepreneurs

Business owners

Commission-based careers

Someone who spent their 20s and early 30s in training or building a business may accumulate wealth more rapidly after 40.

Housing Choices

Real estate decisions also play a major role. A homeowner who purchased property in a fast-growing housing market may accumulate substantial home equity, increasing net worth. Meanwhile, someone renting in a high-cost city may have less net worth but more investment flexibility.

Cost of Living Differences

A household earning $120,000 in a high-cost city may struggle to save aggressively.

That same income in a lower-cost area may allow significant annual savings.

Location plays a major role in wealth accumulation.

A More Useful Way to Evaluate Your Finances at 40

Instead of focusing only on a static net worth number, it’s often more useful to evaluate a broader set of factors.

Here are several questions that can provide a clearer picture of financial health.

What Is Your Savings Rate?

Your savings rate — the percentage of your income that you save or invest each year — is one of the most powerful predictors of future wealth.

Someone saving 20–30% of their income consistently can make significant financial progress even if their starting net worth is modest.

How Stable Is Your Income?

Income stability matters just as much as current net worth.

A household earning $180,000 with strong job security may have far greater long-term financial potential than someone with a volatile income stream.

What Are Your Fixed Expenses?

Housing costs, childcare, and debt obligations heavily influence financial flexibility.

Lower fixed expenses often allow faster wealth accumulation over time.

How Much Are You Investing Annually?

The amount you invest each year is one of the most important drivers of future net worth.

For example, someone investing:

$25,000 annually

earning a 7% average return

could accumulate more than $500,000 over the next decade.

Annual investment contributions matter more than where you started.

Net Worth Scenarios at Age 40

To better understand how different financial situations might play out, it’s helpful to consider a few hypothetical scenarios. These examples illustrate how net worth interacts with income and savings behavior.

Scenario A: Moderate Net Worth With Steady Savings

Age: 40

Income: $90,000

Net worth: $220,000

Annual investment contributions: $15,000

In this case, the individual may feel behind compared with the 3x salary benchmark.

However, investing $15,000 annually could lead to significant wealth accumulation over the next 20–25 years. With steady market returns, this person could easily reach retirement with over $1 million in assets.

Scenario B: High Net Worth but Low Savings Rate

Age: 42

Income: $180,000

Net worth: $700,000

Annual investment contributions: $5,000

Despite a strong starting net worth, limited ongoing savings could slow future growth. In this case, increasing annual investments may matter more than the existing asset base.

Scenario C: Late Start but Strong Income

Age: 40

Income: $150,000

Net worth: $120,000

Annual investments: $35,000

Even though net worth appears modest, aggressive investing combined with a strong income can rapidly close the gap. Within 15–20 years, this person could build a substantial investment portfolio.

What Actually Matters More Than Your Net Worth at 40

While net worth is useful, several other financial factors often matter more when evaluating long-term financial health.

Investment Strategy

Consistent investing in diversified assets such as index funds or ETFs can significantly influence long-term wealth. Asset allocation and discipline often matter more than timing the market, so get in the habit of contributing to an investment fund regularly.

Debt Levels

High-interest debt can slow wealth accumulation.

Reducing credit card balances or high-interest loans can improve financial flexibility.

Income Growth Potential

Future earning power can significantly influence wealth outcomes.

Many professionals reach peak income levels in their 40s and 50s.

Financial Flexibility

Flexibility comes from a combination of:

Low fixed expenses

Healthy savings

Manageable debt

Stable income

This flexibility allows individuals to adapt to career changes or unexpected events.

Can You Catch Up Financially After 40?

One of the most common concerns people have when evaluating their net worth is whether they are “too far behind.” The reality is that many individuals significantly accelerate wealth accumulation after 40. Several factors contribute to this.

Peak Earning Years

For many professionals, income rises significantly during their 40s and 50s.

Higher income can support larger investment contributions.

Reduced Early-Career Expenses

Student loans, childcare costs, and housing instability often decline over time.

These changes free up additional resources for saving and investing.

Compounding Investment Returns

The longer investments remain in the market, the more compounding can work in your favor. Even modest contributions can grow substantially over time.

For these reasons, someone with a modest net worth at 40 may still build significant wealth before retirement.

Financial Goals for Your 40s

Instead of focusing solely on net worth benchmarks, it can be more helpful to set financial priorities for this decade.

Strengthen Retirement Savings

Maximizing retirement contributions can significantly improve long-term financial security.

Evaluate Housing Costs

Housing is often the largest expense for most households. Ensuring housing costs align with long-term financial goals is important.

Increase Investment Contributions

Higher contributions during peak earning years can dramatically improve future outcomes. I personally use Fidelity for all of my investments. You can manage the accounts yourself, or Fidelity offers professionally managed accounts.

Build Financial Resilience

Maintaining emergency savings and manageable debt levels provides stability during unexpected events.

The Bigger Picture

Net worth benchmarks can provide useful context, but they rarely tell the full story. By age 40, many people have experienced career changes, financial setbacks, or major life transitions that affect their financial position.

What matters most is not whether you meet a specific benchmark today. What matters is your financial trajectory — the direction your finances are moving over the next 10–20 years.

If you are consistently saving, investing, and making thoughtful financial decisions, your long-term outlook may be stronger than you think.